Businesses must understand the SB 253 and SB 261 timeline as California’s climate compliance clock ticks, with mandatory emissions and risk reporting starting in 2026.

This timeline breaks down the major deadlines, what’s required, and how to prepare.

| Date | Requirement |

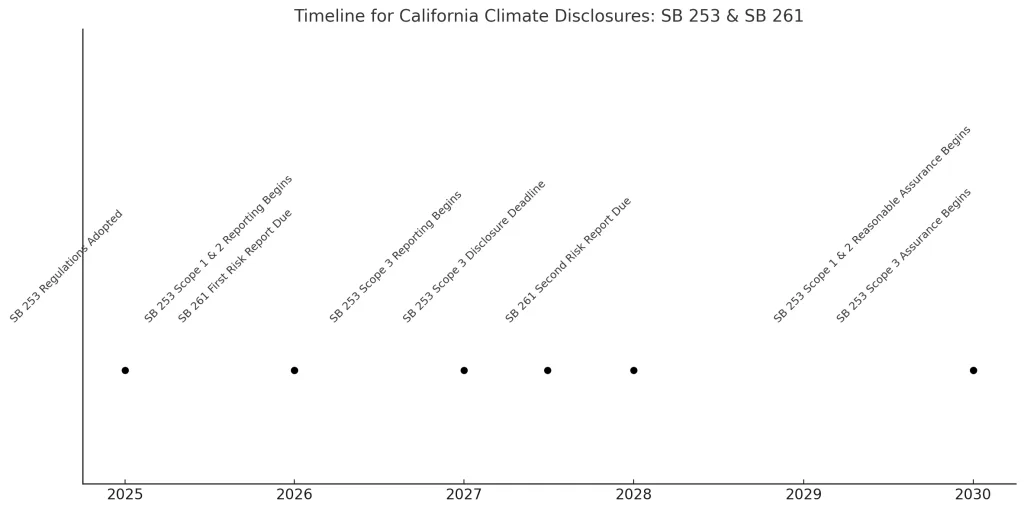

| Jan 1, 2025 | SB 253 regulations must be adopted |

| Jan 1, 2026 | First SB 253 Scope 1 & 2 disclosures due |

| Jan 1, 2026 | First SB 261 risk report due |

| 2027 (mid-year) | SB 253 Scope 3 disclosures begin (180 days after Scope 1 & 2) |

| 2030 | Reasonable assurance required for Scope 1, 2, and Scope 3 emissions |

SB 253 and SB 261 timeline reporting requirements demand companies with $1B+ in annual revenue doing business in California disclose emissions annually.

Applies to: Companies with $1B+ in annual revenue doing business in California

What’s required: Annual public disclosure of Scope 1, 2, and 3 GHG emissions

Standard: Greenhouse Gas Protocol

Assurance: Third-party limited (then reasonable) assurance required

| Year | Disclosure | Notes |

| 2025 | CARB adopts implementing rules | Deadline: Jan 1, 2025 |

| 2026 | First Scope 1 & 2 reporting | Must follow GHG Protocol |

| 2027 | First Scope 3 reporting | Due within 180 days after Scope 1 & 2 |

| 2030 | Reasonable assurance begins | For Scope 1, 2, and 3 (if required) |

Applies to: Companies with $500M+ in revenue doing business in California

What’s required: Biennial climate-related financial risk reports

Standard: TCFD (or equivalent, e.g. ISSB)

Disclosure: Public on company’s website

| Year | Disclosure | Notes |

| 2026 | First report due | Deadline: Jan 1, 2026 |

| 2028 | Second report due | Continues every two years |

Here’s your checklist if you’re likely subject to SB 253 or SB 261:

Set up an internal SB 253 and SB 261 timeline tracker to stay ahead of deadlines and prepare for assurance provider engagement. Contact us for a walkthrough or book a demo.