As the global economy accelerates toward sustainability, financial statements alone no longer tell the full story. Financed emissions, the carbon footprint of loans, investments, and underwriting, now dominate institutional climate impacts. Investors, regulators, and stakeholders demand transparent, comparable disclosures on how businesses and particularly financial institutions manage these emissions.

At the core of this shift are the IFRS S1 and S2 standards developed by the ISSB, extended to sustainability disclosures, along with the newly launched SBTi Financial Institutions Net-Zero Standard (July 2025). These frameworks, together with TCFD, GRI, and principles from UNEP FI and PRI, are rapidly becoming essential tools for measuring and managing financed emissions.

IFRS S1 and S2: Driving Credible Financed Emissions Reporting

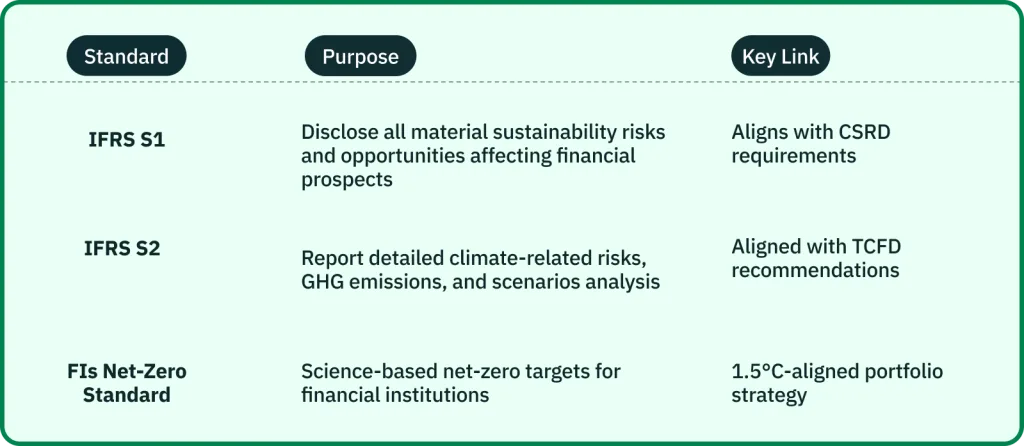

IFRS S1 sets the foundation by requiring disclosure of sustainability-related risks and opportunities, including financed emissions, when they affect enterprise value. This aligns with emerging global disclosure mandates such as the EU’s CSRD, ESRS, and SFDR, as well as the US SEC’s climate disclosure rules.

IFRS S2 aligns climate-related disclosures with TCFD recommendations and the GHG Protocol. This harmonization supports consistent financed emissions assessment across frameworks like GRI and the EU Taxonomy, reinforcing transparency and comparability.

The new SBTi Financial Institutions Net-Zero Standard equips financial institutions with a science-based roadmap to align lending, investment, underwriting, and capital market activities with 1.5 °C pathways to achieve net-zero by 2050. It builds on initiatives by the NZBA and complements near-term guidance under the SBTi framework.

Global Journey Toward Responsible Financing

Regulatory bodies worldwide, including the EU, UK, Asia-Pacific, and North America, are advancing mandatory sustainability disclosures. India’s SEBI, Singapore’s MAS, Hong Kong’s HKMA, and the US SEC are incorporating financed emissions into regulatory frameworks, often using ISSB and GRI as foundations.

Financial institutions across regions are adopting Science-Based Targets. However, ambition must be matched with credible disclosure. IFRS S2 and the new SBTi standard provide transparent, standardized methods to report climate strategies and carbon-financed exposure in line with TCFD, GRI, and evolving national requirements.

SBTi Update: Net-Zero Standard for Financial Institutions

On 22 July 2025, the SBTi released its FIs Net-Zero Standard. This robust, science-based framework enables lenders, asset managers, insurers, and banks to set financed emissions targets across portfolios and align financial flows with net-zero 2050 goals.

It complements the existing Near-Term Criteria (2024), empowering financial firms to move beyond disclosure toward portfolio-wide decarbonization across listed equities, debt, project finance, and private assets.

The Road Ahead: Integration and Innovation

Global markets are converging around IFRS S1 and S2 as a baseline for credible, comparable sustainability disclosures. GRI remains a vital parallel standard, ensuring coverage of broader ESG topics and stakeholder expectations. EU policies such as CSRD and SFDR and taxonomies from regions like ASEAN and Latin America are reinforcing this convergence.

Digital tools like XBRL, automated assurance, and AI-powered analytics are transforming ESG and financed emissions reporting, making it more granular, verifiable, and decision-useful. Regulators such as SEBI, and SEC are enabling digital compliance infrastructure to support these advancements.

Unified Future in Finance and Sustainability Reporting

Financial institutions must now integrate financial and sustainability reporting into a single narrative centered on financed emissions. IFRS S1 and S2, aligned with ISSB, TCFD, GRI, SFDR, the EU Taxonomy, and the new SBTi net-zero framework, offer powerful tools to measure, strategize, and disclose climate impact through financing activity:

Measure financed emissions and allocate financed-carbon risk across portfolios

Target short- and long-term financed emission reductions aligned with IFRS, SBTi, and regulatory expectations

Report transparently to investors, regulators, and stakeholders.

This isn’t just compliance. It’s a strategic imperative. Early adopters of financed emissions disclosure and net-zero financing targets will gain trust, unlock capital, and future-proof their institutions in a rapidly transitioning global market.

Sprih helps financial institutions operationalize financed emissions disclosures—fast. From IFRS S2-aligned data models to audit-ready reporting workflows and SBTi-compatible tracking across lending, investing, and underwriting, Sprih’s platform is purpose-built for the next era of climate accountability in finance.

Financed emissions refer to the greenhouse gas emissions linked to a financial institution’s lending, investment, and underwriting activities. These emissions represent the carbon footprint that results indirectly from capital allocation decisions.

Why are financed emissions a focus in sustainability reporting?

Financed emissions often make up the majority of a financial institution’s climate impact. Regulators, investors, and frameworks like IFRS S2, TCFD, and SBTi now treat them as critical to understanding an institution’s climate exposure, risk, and accountability.

What is the role of IFRS S1 and S2 in financed emissions reporting?

IFRS S1 requires disclosure of sustainability-related risks and opportunities when material to enterprise value, including those related to financed emissions. IFRS S2 focuses specifically on climate-related disclosures, aligning with TCFD and enabling consistent emissions and risk reporting across financial institutions.

What is the new SBTi Net-Zero Standard for Financial Institutions?

Released in July 2025, this standard enables financial institutions to set science-based targets for portfolio-level emissions reductions. It guides banks, asset managers, and insurers in aligning their capital flows with a 1.5°C net-zero pathway, covering listed equities, bonds, project finance, and private assets.

Can these disclosures align with multiple global standards?

Yes. IFRS S1 and S2 are designed to harmonize with frameworks like TCFD, GRI, SFDR, and the EU Taxonomy. With the release of the SBTi Net-Zero Standard for Financial Institutions, financial entities can create unified, credible disclosure strategies across jurisdictions.