California’s climate law influence is no longer theoretical—it’s active, visible, and reshaping both U.S. policy and corporate behavior worldwide. One that’s already nudging federal agencies, reshaping corporate norms, and setting the tone for other states and countries. These laws could be the tipping point that shifts voluntary ESG into mandatory infrastructure nationwide.

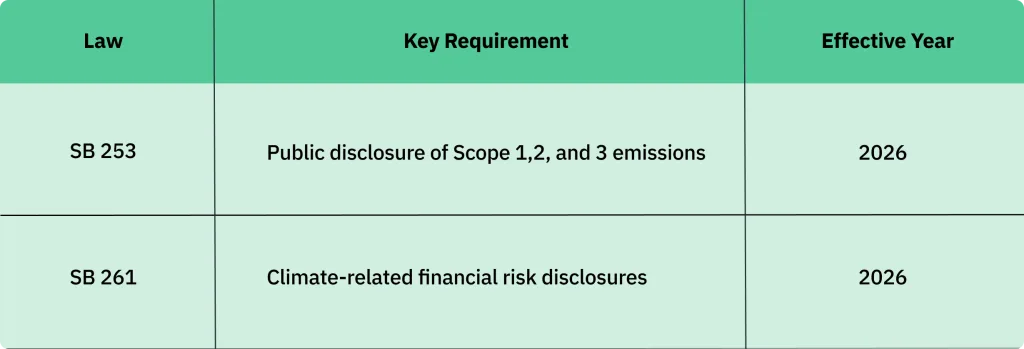

California accounts for nearly 15% of the U.S. economy. If it were a country, it would be the fifth-largest economy in the world. When it enacts laws like SB 253 (corporate emissions disclosure) and SB 261 (climate risk reporting), those rules apply to thousands of national and global companies doing business in the state.

This isn’t just state-level compliance. It’s de facto national influence.

Both laws require companies to treat climate data the way they treat financials—traceable, third-party assured, and publicly available.

These laws go further than what the SEC currently mandates. And they apply to both public and private companies. That’s already setting a new compliance bar.

For years, ESG reporting lived in the realm of voluntary disclosures—GRI, CDP, TCFD, SASB. That’s changing.

California’s legislation shows how voluntary frameworks can become legal requirements. SB 253 uses the GHG Protocol. SB 261 aligns with TCFD. These aren’t new tools—they’re just being enforced now.

That model—voluntary guidance, followed by mandatory uptake—is exactly how financial accounting standards evolved. Climate disclosure is on the same path.

The SEC’s final climate rule marks a milestone, but many believe it will tighten over time. Meanwhile:

The direction is clear: climate data is infrastructure, and federal regulation is catching up.

California may be the first U.S. state to pass climate disclosure mandates of this scope—but it likely won’t be the last. Here’s where pressure is already building:

As more states align, the cost of non-standardization will grow—and a national baseline will become the pragmatic solution.

Most large companies don’t report to just one jurisdiction. They operate across state lines and continents. They don’t want 12 formats for 12 rules.

So even if climate laws vary today, businesses are already building systems that:

This isn’t reactive compliance. It’s strategic alignment.

Here’s what happens when climate disclosure becomes public, comparable, and credible:

Companies that move early gain trust. Companies that lag face rising costs and reputational drag.

Even without a national mandate yet, the incentives to act like there is one are already real.

It’s not just the U.S. watching California.

| Jurisdiction | Disclosure Type | Applies To | Timeline | Standard Used |

|---|---|---|---|---|

| California (SB 253) | GHG Emissions (Scope 1, 2, 3) | $1B+ revenue companies doing business in CA | 2026 | GHG Protocol |

| SEC (US) | Scope 1 & 2 (Scope 3 optional) | Public companies | 2026 (phased) | TCFD |

| EU (CSRD) | Emissions, risk, value chain impact | Large listed & unlisted firms | 2024-2028 | ESRS |

California may not write global ESG law, but its regulations shape the operational and data infrastructure of the global economy.