For asset managers, banks, insurance companies, and pension funds, scope 3 category 15 investments financed emissions is the elephant in the room. While operational emissions (Scope 1 and 2) are typically measured in thousands of tons of CO2e, financed emissions often dwarf them by hundreds or thousands of times.

A $100 billion asset manager with 500 employees might have operational emissions of 5,000 tons CO2e, but scope 3 category 15 investments financed emissions exceeding 10 million tons CO2e. That gap is precisely why regulators, investors, and net-zero frameworks are demanding financial institutions measure and disclose Category 15.

This guide covers the GHG Protocol definition of Category 15, calculation methodologies by asset class, data challenges, and how to build a sustainable investment program around financed emissions measurement.

Scope 3 Category 15 (Investments) captures the greenhouse gas emissions from the companies, projects, and assets you have a financial stake in. This includes:

The key principle: If your capital is deployed into an asset and that asset generates emissions, those financed emissions are your reporting responsibility under GHG Protocol.

Consider the scale difference:

A bank with $500 billion in lending might have:

That’s a ratio of 1:5,000 or worse. For asset managers, the ratio is often even more extreme.

This matters because it tells you where the real climate risk and impact are. If you’re a financial institution, your material climate footprint is almost entirely through the capital you deploy, not your office operations.

Regulators, the net-zero asset manager initiative (NZAM), the Task Force on Climate-related Financial Disclosures (TCFD), and institutional investors have figured this out. They now require financial institutions to measure and disclose financed emissions and set reduction targets.

The GHG Protocol Scope 3 Standard defines Category 15 at a high level: financed emissions from investments.

The Partnership for Carbon Accounting Financials (PCAF) provides detailed guidance on how to calculate financed emissions. PCAF is the industry standard for financial institutions and has become the de facto methodology for Category 15 reporting.

PCAF includes:

For practical purposes, if you’re a financial institution measuring Category 15, you’re almost certainly using PCAF methodology. GHG Protocol and PCAF are complementary, not competitive.

For stocks and bonds, the most common methodology is economic value attribution (EVA) or enterprise value including cash (EVIC) approach:

Formula: Financed Emissions = Investee Company Emissions × (Your Investment Value / Investee’s Total Enterprise Value or Market Capitalization)

Example:

The challenge is obtaining emission data from investees, especially if they don’t publicly report. For non-reporting companies, financial institutions use estimated emissions based on revenue and industry benchmarks.

For infrastructure, energy, and development projects, you typically receive emissions data directly from the project operator, or you calculate based on project specifications:

Formula: Your Financed Emissions = Project Total Emissions × (Your Share of Project Finance / Total Project Cost or Capacity)

Example:

Project-based financed emissions are often lower than operational emissions because you’re amortizing construction impacts over the asset’s life, and renewable projects generate emissions offsets during operation.

For properties (investment real estate, mortgages), emissions are typically measured using:

Formula: Financed Emissions = Property Emissions Intensity (tons CO2e/m²) × Floor Area × Your Share of Financing/Ownership

Example:

Real estate emissions are easier to measure than other asset classes because building energy data is relatively standardized and often available from property managers.

For PE and private company investments, you often have direct access to operational data or can work with portfolio companies to collect it. Methodologies are the same as listed equity, but data collection is more collaborative and requires deeper engagement with portfolio company management.

The biggest obstacle to Category 15 reporting is data availability and quality:

Challenge 1: Investee companies don’t report emissions

Challenge 2: Uneven data quality across asset classes

Challenge 3: Attribution complexity

Challenge 4: Scope scope inconsistency

Challenge 5: Timing and restatement

Financial institutions are measuring Category 15 because regulation demands it:

TCFD (Task Force on Climate-related Financial Disclosures):

IFRS S2 (Sustainability Disclosure Standard):

EU Sustainable Finance Disclosure Regulation (SFDR):

APRA (Australia):

BRSR and Local Standards:

Net-Zero Asset Manager Initiative (NZAM):

The bottom line: Category 15 disclosure is no longer optional for large financial institutions. It’s becoming a minimum requirement for regulatory compliance, investor relations, and market credibility.

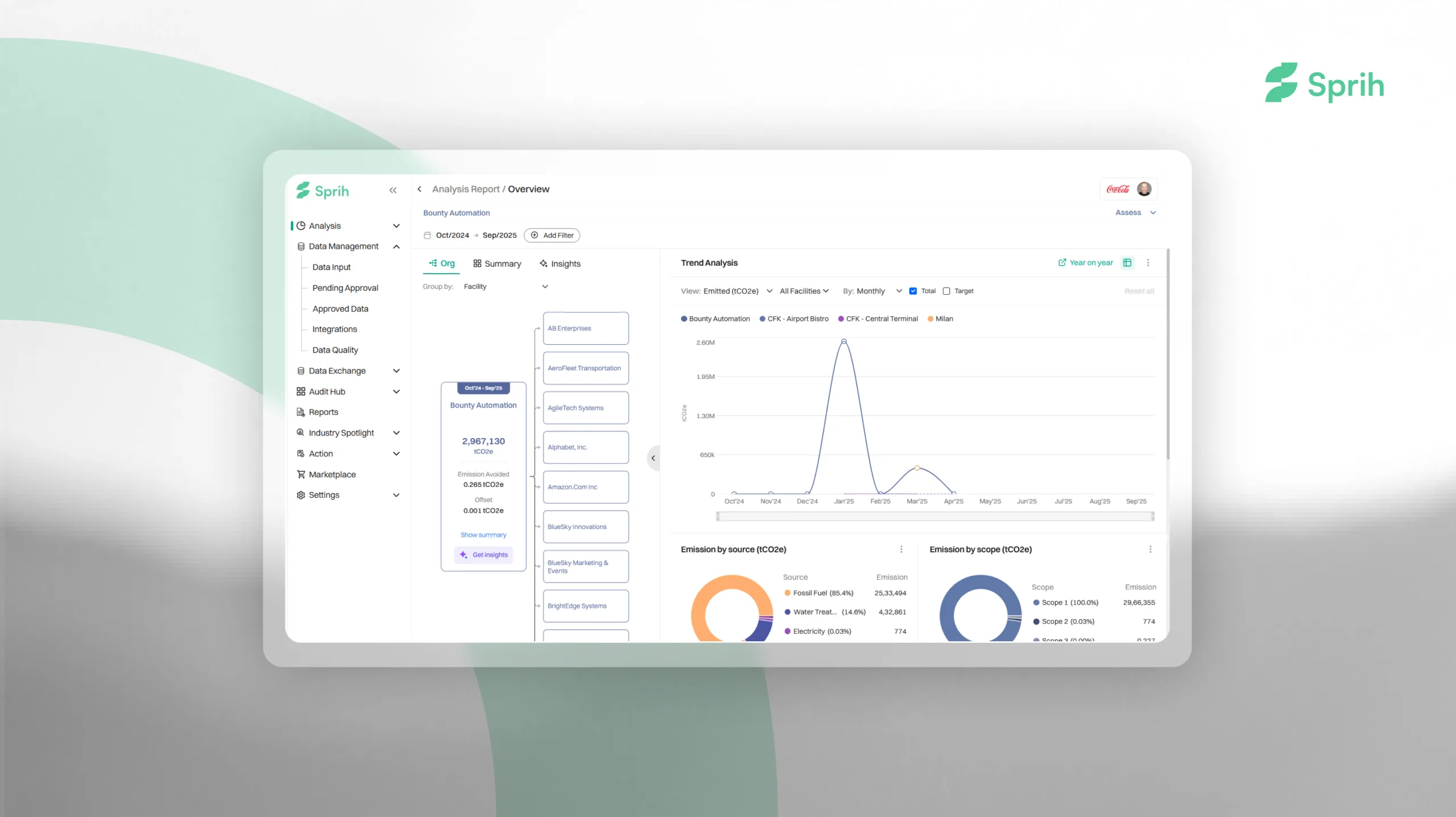

Given the complexity of Category 15—multiple asset classes, inconsistent investee data, regulatory compliance—most institutional investors rely on sustainability software to aggregate and manage portfolio-level emissions data.

A robust platform should:

For financial institutions tracking scope 3 category 15 investments financed emissions, Sprih’s carbon accounting software provides PCAF-aligned calculation workflows across all asset classes. Learn how Sprih’s AI-native sustainability platform helps banks and asset managers move from manual financed emissions tracking to automated, audit-ready disclosure.

For financial institutions, Scope 3 Category 15 isn’t a compliance burden—it’s the measure of your actual climate impact. The capital you deploy into companies, projects, and assets drives real-world emissions. Measuring financed emissions isn’t just good sustainability practice; it’s essential for understanding and managing climate risk in your portfolio.

Building a robust Category 15 measurement program requires cross-functional engagement: investment teams, risk management, sustainability, and finance. It requires data infrastructure to aggregate emissions from dozens or thousands of investees. And it requires ongoing refinement as methodologies, regulations, and your portfolio evolve.

Learn more about scope 3 category 15 investments financed emissions with resources from PCAF Standard and NZBA guidance.

Get started with carbon accounting software designed for financial institutions.

Ready to establish financed emissions reporting across your portfolio? Sprih’s enterprise platform supports financial institutions in automating Scope 3 Category 15 measurement, scenario modeling, and regulatory compliance. Request a demo to see how we can accelerate your financed emissions program.