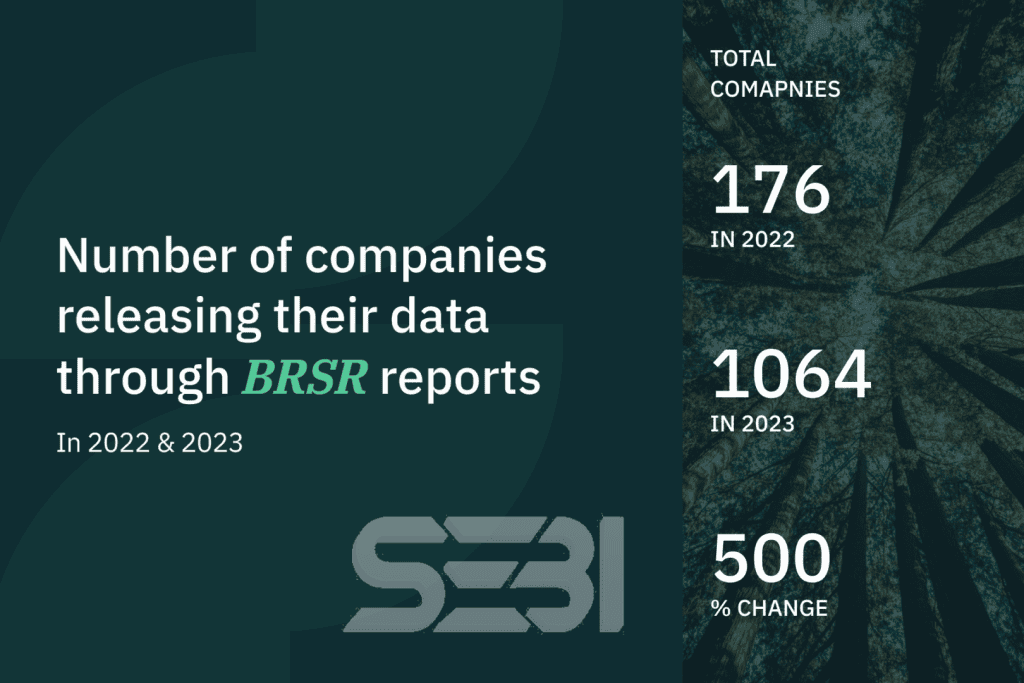

There is a growing demand from investors and various stakeholders for companies to provide comprehensive disclosure regarding their carbon footprint, reduction targets, risk management practices, and overall environmental, social, and governance (ESG) impacts. The rollout of SEBI’s BRSR framework in its inaugural year witnessed a lukewarm response, with a mere 176 companies disclosing their ESG data. However, starting from the fiscal year 2022-2023, a significant shift occurred as the top 1000 listed companies were required to report their ESG metrics. This mandate sparked remarkable engagement, evidenced by 1064 companies submitting their Business Responsibility and Sustainability Report (BRSR), as reported on the India National Stock Exchange website.

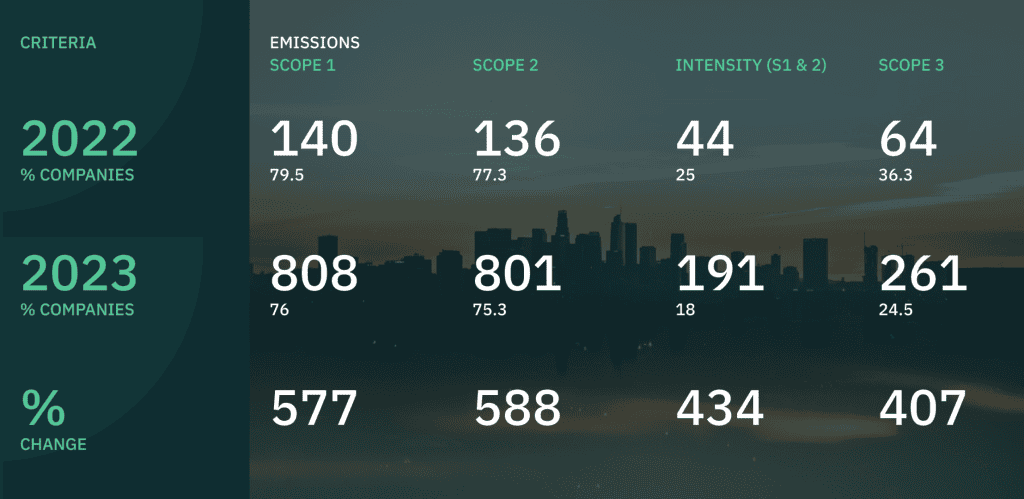

Achieving a reduction in Scope 3 Greenhouse Gas (GHG) emissions is crucial for reaching the global net zero target by 2050, as these emissions typically constitute 60-90% of a company’s total emissions. Unlike Scope 1 and Scope 2 emissions, Scope 3 emissions occur outside the company, encompassing the supply chain, upstream, and downstream activities.

Although disclosure requirements for Scope 3 reporting are currently voluntary, understanding and addressing these emissions are essential for managing transition risks, evaluating investment risks, and seizing opportunities to enhance efficiency, reduce costs, and bolster resilience.

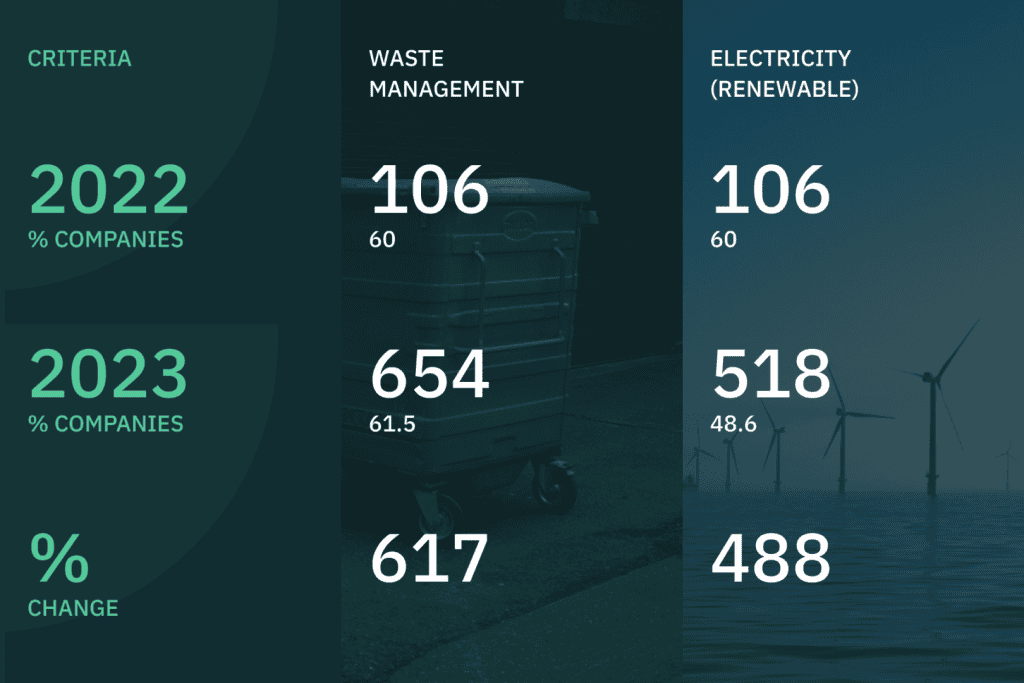

Electricity usage typically constitutes the primary contributor to Scope 2 emissions, a mandatory data field in BRSR reporting. In 2023, only 35 companies did not report electricity data. To mitigate emissions associated with electricity consumption, many companies are transitioning to renewable energy sources such as solar and wind power.

When it comes to waste management, companies are now required to adhere to specific procedures for managing and accounting for emissions associated with waste generated during operations. This mandate necessitates companies to meticulously track and quantify the emissions resulting from the disposal and treatment of waste materials produced as a byproduct of their activities. Compliance with these regulations ensures that companies effectively manage their environmental impact, mitigate pollution, and contribute to sustainable waste management practices mandated by regulatory authorities.

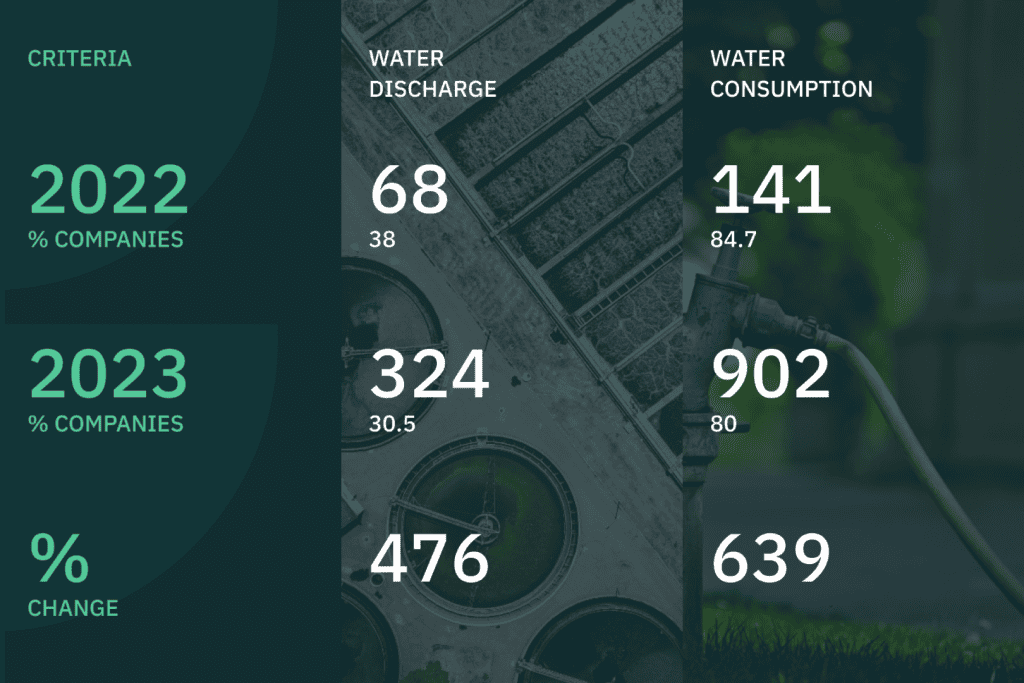

Water consumption and discharge by industries pose significant challenges, yet only a limited number of companies report their water discharge data. Another pressing concern is the extraction of fresh water from groundwater sources. In BRSR framework, companies are required to disclose the source of water extraction. This information is crucial for assessing the environmental impact of industrial activities, ensuring responsible water management practices, and safeguarding water resources. This disclosure also enables stakeholders to evaluate the potential risks associated with water scarcity, pollution, and depletion, and encourages companies to adopt measures for conserving water resources and minimizing environmental impact.

The BRSR framework, established by SEBI, mandates India’s top 1000 listed companies to disclose their Environmental, Social, and Governance (ESG) metrics, enhancing transparency and aligning with global sustainability standards.

How has company participation in BRSR reporting evolved since its inception?

Initially, only 176 companies disclosed ESG data under the BRSR framework. However, following SEBI’s mandate, participation surged to 1064 companies by the fiscal year 2022-2023.

Why is Scope 3 emission reporting significant in the BRSR framework?

Scope 3 emissions, encompassing indirect emissions from a company’s value chain, often constitute 60-90% of total emissions. Addressing these is crucial for companies aiming for net-zero targets by 2050.

What are the mandatory environmental disclosures under the BRSR framework?

Companies are required to report on electricity consumption (Scope 2 emissions), waste management practices, and water usage and discharge, ensuring comprehensive environmental accountability.

How does the BRSR framework enhance corporate sustainability practices?

By standardizing ESG disclosures, the BRSR framework enables companies to identify areas for improvement, align with sustainability goals, and build trust with stakeholders through transparent reporting.