“ESG reporting has evolved from a corporate social responsibility initiative launched by the United Nations into a global phenomenon in less than two decades.”

BRSR compliance is now a legal requirement for India’s largest listed companies — and the scope is expanding. The Business Responsibility and Sustainability Reporting (BRSR) framework, introduced by SEBI, mandates that the top 1,000 listed companies report on their environmental impact, social responsibilities, and governance practices. This guide covers what BRSR requires, who it applies to, and how the framework has evolved since 2011.

Why BRSR Was Needed

Traditionally, corporate reporting focused on financial performance. Investors, regulators, and communities had no standardized way to evaluate whether a company’s operations were sustainable, ethical, or socially responsible. Globally, this gap led to greenwashing, where companies made sustainability claims without real data to back them.

In India, the BRR (Business Responsibility Report) had existed since 2012 but had a limited scope, inconsistent formats, and no assurance requirements. A 2018 IICA-UNICEF study showed these gaps, stating that information disclosed by companies was often incomplete or unclear. BRSR was developed to address these issues.

Objectives

- Embed ESG into operations: Move sustainability from a peripheral compliance activity to a core part of how companies operate, invest, and make decisions.

- Standardize non-financial disclosure: Ensure sustainability information is consistent and comparable across companies, making it actually useful to investors and analysts.

- Align with international standards: Bring Indian corporate ESG disclosures in line with GRI, SASB, TCFD, and IFRS S1 & S2, enabling cross-border benchmarking.

- Build stakeholder trust through transparency: Give investors, regulators, employees, and communities reliable, independently assured ESG data to make informed decisions.

Evolution

India’s journey to BRSR spans over a decade — from voluntary guidelines in 2011 to mandatory, independently assured reporting in 2023.

YEAR — MILESTONE

WHAT HAPPENED

2011

National Voluntary Guidelines (NVG)

MCA releases nine principles for responsible business conduct covering ESG dimensions. Voluntary in nature; forms the conceptual backbone for all future frameworks.

2012

BRR Introduced (Top 100)

SEBI makes it mandatory for the top 100 listed entities by market cap to file a BRR aligned with NVG principles. India becomes an early mover in mandating ESG disclosure.

2013

Companies Act, Section 135

Mandatory CSR spending introduced for qualifying companies. Social responsibility embedded into corporate law for the first time in India.

2015

BRR Expanded (Top 500)

SEBI extends BRR applicability to the top 500 listed companies. The UN General Assembly simultaneously adopts the 17 Sustainable Development Goals, a framework BRSR’s principles later map to.

2018

IICA-UNICEF Study

The study found fundamental gaps in BRR: information was inconsistent, incomplete, and unverified. This directly led to the development of BRSR.

2019

BRR Expanded (Top 1,000) + NGRBC

SEBI scales BRR to 1,000 companies. MCA releases updated NGRBC, the revised nine-principle framework that BRSR is built upon.

2021

BRSR Introduced

SEBI replaced BRR with BRSR in May 2021, mandating the top 1,000 listed entities to report from FY 2022–23. First time both qualitative and quantitative ESG disclosures are required together.

2023

BRSR Core Launched

SEBI introduces BRSR Core, a focused sub-set with 9 ESG KPI attributes requiring mandatory third-party assurance, phased across companies by net worth through FY 2026–27.

Who Needs to Comply with BRSR

BRSR compliance is governed by SEBI’s LODR (Listing Obligations and Disclosure Requirements) Regulations. The primary obligation falls on India’s largest listed companies, with applicability structured in two tiers.

Tier 1: Full BRSR (mandatory from FY 2022–23)

All top 1,000 listed entities by market capitalization are required to file a full BRSR report as part of their annual reports submitted to SEBI. This has been mandatory from the financial year 2022–23 onwards.

Tier 2: BRSR Core with mandatory assurance (phased rollout)

BRSR Core is a more demanding sub-framework requiring independent third-party assurance on a focused set of KPIs. It is being phased in as per SEBI Circular, July 12, 2023.

FINANCIAL YEAR

BRSR CORE MANDATORY FOR

FY 2023–24

Top 150 listed entities by market capitalization

FY 2024–25

Top 250 listed entities by market capitalization

FY 2025–26

Top 500 listed entities by market capitalization

FY 2026–27

Top 1,000 listed entities by market capitalization

Value chain disclosure

Under BRSR Core, listed entities are also required to obtain disclosures from their value chain partners — suppliers, contractors, and distributors — extending ESG accountability beyond a company’s own operations. This makes BRSR a supply-chain governance tool, not just a corporate reporting requirement.

Voluntary adoption of BRSR

SEBI encourages all other listed companies outside the top 1,000 to adopt BRSR voluntarily. Voluntary adoption demonstrates responsible intent, prepares for future regulatory expansion, and builds credibility with institutional investors who increasingly screen ESG data regardless of company size.

Why BRSR Matters

BRSR creates value for three distinct groups: the companies filing it, the investors evaluating it, and the employees and wider stakeholders affected by corporate conduct.

PARAMETER

COMPANY

INVESTOR

EMPLOYEE & STAKEHOLDER

Risk

Identifies operational risks like environmental impact, safety gaps, and supply chain issues early

Helps evaluate hidden ESG risks before investing

Highlights workplace risks, safety conditions, and community impact

Transparency

Improves disclosure quality and builds trust with SEBI

Provides clear, comparable ESG data for decision-making

Gives visibility into company practices affecting employees and communities

Decision-Making

Supports better internal strategy and long-term planning

Enables informed investment and portfolio decisions

Helps stakeholders make informed employment and consumption choices

Credibility

Strengthens brand trust and corporate reputation

Increases confidence through reliable, assured data

Builds trust in how companies operate and report

Performance

Improves efficiency by tracking energy, water, and resources

Helps assess long-term company performance beyond financials

Reflects company commitment to employee well-being and social impact

Global Alignment

Aligns with frameworks like GRI and TCFD

Enables comparison with global peers

Connects company actions with United Nations Sustainable Development Goals

Structure of BRSR

The BRSR report is split into three sections: company basics, how sustainability is managed, and the actual performance results.

Section A — General Disclosure

Reporting Entity Identity & Context

- → Company details, products and services, operational footprint, employee numbers

- → CSR details, transparency compliance

- → Reporting boundary: standalone or consolidated

Section B — Management & Process Disclosure

Governance Systems Behind ESG Commitments

- → Policies, targets, and oversight mechanisms for each of the nine NGRBC principles

- → Board-level accountability and internal control systems

Section C — Principle-wise Performance Disclosure

Measured ESG Outcomes Across All Nine Principles

- → Essential Indicators: Mandatory quantitative and qualitative data required of all companies

- → Leadership Indicators: Voluntary advanced disclosures for companies with mature ESG practices

- → Covers all nine NGRBC principles — from ethical governance to consumer responsibility

The 9 Principles of BRSR

BRSR’s Section C reporting is structured around the nine principles of the National Guidelines for Responsible Business Conduct (NGRBC).

The 9 NGRBC Principles — BRSR Section C

P1

Ethical Governance

Businesses should conduct and govern themselves with integrity, in a manner that is ethical, transparent, and accountable.

P2

Sustainable Products & Services

Businesses should provide goods and services in a manner that is sustainable and safe.

P3

Employee Well-Being

Businesses should respect and promote the well-being of all employees, including those in their value chains.

P4

Stakeholder Responsiveness

Businesses should respect the interests of and be responsive to all their stakeholders.

P5

Human Rights

Businesses should respect and promote human rights.

P6

Environmental Protection

Businesses should respect and make efforts to protect and restore the environment.

P7

Public Policy Engagement

When engaging in public and regulatory policy, businesses should do so in a manner that is responsible and transparent.

P8

Inclusive Growth

Businesses should promote inclusive growth and equitable development.

P9

Consumer Responsibility

Businesses should engage with and provide value to their consumers in a responsible manner.

*Each principle requires disclosure under two sub-categories: Essential Indicators (mandatory) and Leadership Indicators (voluntary, for companies with mature ESG practices).

“`

Common BRSR Challenges

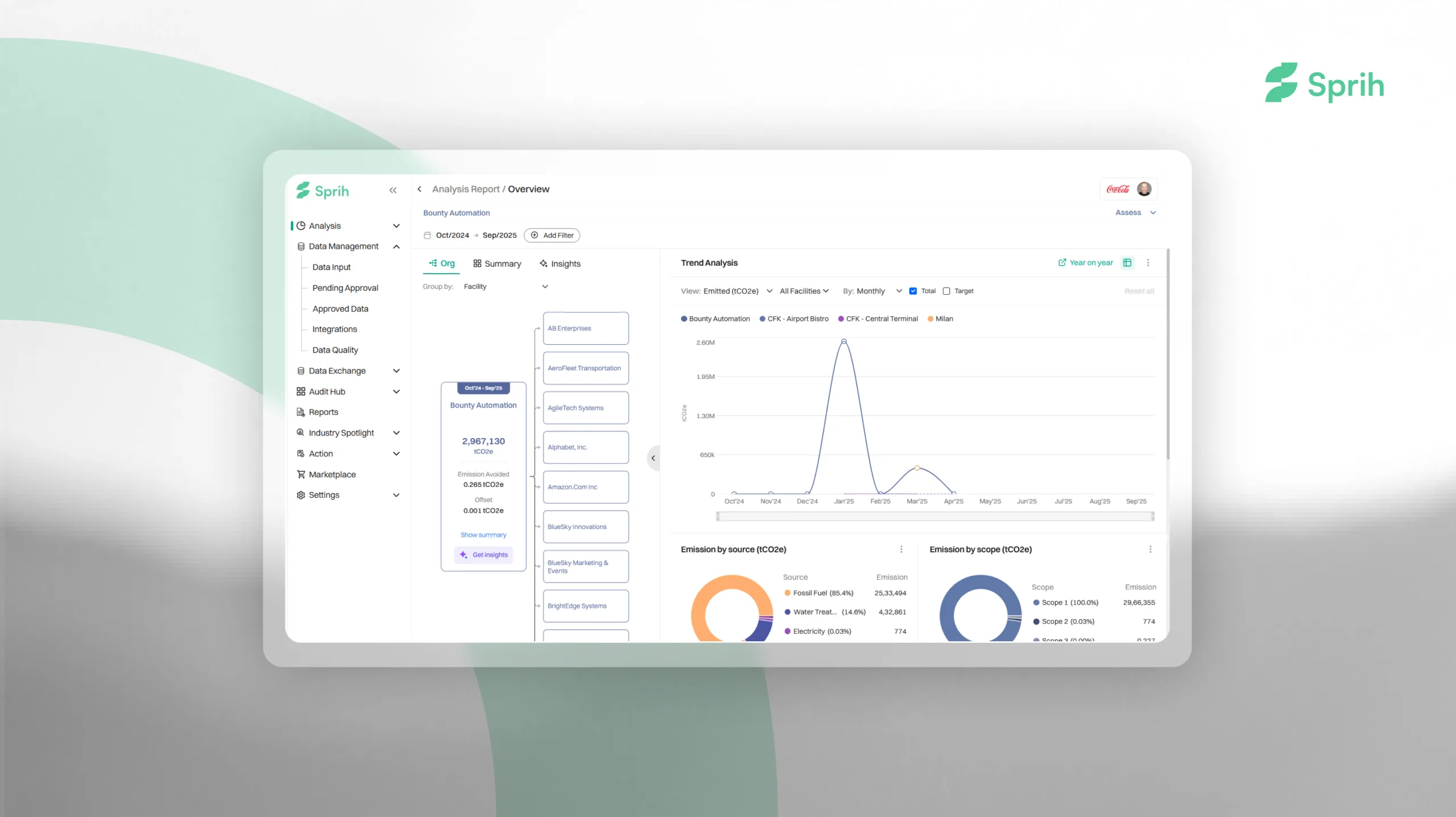

BRSR compliance is complex because ESG data is scattered, inconsistent, and constantly evolving. Companies often struggle with fragmented data across systems, mismatched formats, and the added complexity of collecting information from suppliers. Preparing for assurance and keeping up with changing requirements from the Securities and Exchange Board of India (SEBI) further increases the effort.

Most companies filing BRSR are still doing it the hard way — chasing data across systems, following up with suppliers who don’t respond, and hoping the numbers hold up under scrutiny. Sprih automates the parts that drain the most time: ingesting supplier data, normalizing it across formats, and mapping it to the right disclosure categories. The result is a BRSR report you can actually defend — not one you assembled under deadline. Talk to the Sprih team to see how it works in practice.