The sustainability reporting landscape has become fragmented. Your board asks for TCFD reporting. Your investors want GRI. Your EU regulator mandates CSRD (which aligns with ISSB). Your supply chain partners request SASB data. And your lenders ask for metrics specific to your industry.

So which framework do you actually use? The answer, frustratingly, is often “all of them.” But understanding what each framework does, which stakeholders demand it, and how they complement (or overlap with) each other is the first step toward a sustainable reporting strategy.

This guide compares the four dominant GRI SASB TCFD ISSB sustainability reporting frameworks, explains their differences, and shows you how to build a single-dataset, multi-framework reporting approach instead of managing parallel data systems.

Before diving into comparisons, it’s worth understanding why sustainability reporting frameworks proliferated.

Different stakeholder groups have different information needs:

Since these stakeholder groups don’t always align, different frameworks emerged to serve different purposes. The EU built CSRD for compliance. The SASB built their standards for investor decision-making in specific sectors. The TCFD focused narrowly on climate risk. And GRI took a broader, multi-stakeholder approach to impact reporting.

Today, the regulatory pendulum is swinging toward convergence through ISSB (the International Sustainability Standards Board), which aims to harmonize investor-focused standards globally. But full convergence will take years. For now, you need to understand all four.

Purpose: Multi-stakeholder impact reporting (environment, social, governance) Audience: Investors, regulators, NGOs, employees, customers, general public Scope: Broad—covers all sustainability topics Materiality: Double materiality (impact on the world + financial impact on the company) Adoption: Most widely used globally; 10,000+ organizations report

GRI 1 (Foundation), GRI 2 (General Disclosures), and GRI 3–8 (Topic-Specific Standards) cover:

Double Materiality: GRI asks “What matters to the business?” AND “What impact does the business have on the world?” This is intentional—GRI believes companies should report both financial and societal impact.

Comprehensive: GRI covers 40+ distinct topics. This breadth makes it thorough but also demanding.

Stakeholder-focused: GRI explicitly seeks input from employees, community members, and civil society, not just investors.

Industry-neutral: GRI standards apply the same way across all sectors. There are no tech-specific or finance-specific adjustments.

Purpose: Investor-relevant sustainability metrics specific to industry and financial materiality Audience: Investors, lenders, financial analysts Scope: Industry-specific; typically 5–10 key material sustainability factors per industry Materiality: Single materiality (financial impact only) Adoption: Used by 2,500+ companies, particularly in North America

SASB has developed standards for 77 industries across 11 sectors, each identifying the sustainability factors most likely to affect financial performance and enterprise value in that sector. For example:

Industry-specific: SASB identified the sustainability factors that matter most for your business based on investor research, financial analysis, and materiality assessment specific to your sector.

Investor-focused: SASB only includes metrics that have a material link to enterprise value. If an sustainability factor doesn’t affect financial returns, SASB doesn’t require reporting on it.

Comparable across competitors: Because SASB standards apply within industry, you can compare your sustainability performance directly with competitors using the same metrics.

Concise: Most companies report 5–10 SASB metrics, not 40. This makes it less burdensome than GRI but also narrower in scope.

Purpose: Climate risk disclosure aligned with financial reporting Audience: Investors, lenders, regulators Scope: Climate (temperature, GHG, physical risk, transition risk) Materiality: Financial materiality (climate’s impact on enterprise value) Adoption: Recommended by regulators globally; now being absorbed into ISSB

TCFD organizes climate disclosure around four pillars:

Climate-only focus: TCFD doesn’t address social, governance, biodiversity, or other sustainability factors. It’s purely climate.

Forward-looking: TCFD requires scenario analysis—what happens to your business under different climate futures? This is different from backward-looking emissions reporting.

Mandatory in many jurisdictions: TCFD recommendations have been adopted or mandated by stock exchanges, regulators, and governments worldwide.

Transition ready: TCFD explicitly addresses transition risk (stranded assets, policy changes, market shifts) in addition to physical risk (flooding, drought, extreme weather).

Purpose: Global baseline for investor-relevant sustainability disclosure (IFRS S1 General + IFRS S2 Climate) Audience: Investors, regulators, financial markets Scope: Broad (IFRS S1) + Climate (IFRS S2) Materiality: Double materiality (impact materiality + financial materiality) Adoption: New (published late 2023); becoming mandatory in EU, UK, Australia, Singapore, Hong Kong; voluntary in U.S. (for now)

IFRS S1 (General Sustainability Disclosures): Requires disclosure of governance, strategy, risk management, and metrics related to all material sustainability topics (environment, social, governance).

IFRS S2 (Climate-Related Disclosures): Deep-dive climate reporting aligned with TCFD but incorporating IFRS financial reporting principles.

ISSB is built on the back of TCFD (IFRS S2 essentially codifies TCFD) and extends to all material sustainability factors. It’s designed to be the global baseline that other frameworks align with or supplement.

New global baseline: ISSB aims to replace or harmonize with TCFD, GRI, and other standards over time. It’s the IAASB’s push toward a single global sustainability reporting standard.

Investor-focused but double materiality: ISSB incorporates both financial materiality (investor-relevant) and impact materiality (stakeholder impact).

Mandatory in many jurisdictions: EU CSRD requires ISSB alignment. UK, Australia, Singapore, and others are mandating or strongly recommending ISSB.

Connected to financial reporting: ISSB is part of IFRS, the same body that sets financial accounting standards. This integration signals that sustainability data is as important as financial data.

Emerging standard: ISSB standards are still being refined. Climate (S2) is finalized; other topics are still in development.

Yes, significantly.

The four frameworks overlap on several core metrics:

| Metric | GRI | SASB | TCFD | ISSB |

|---|---|---|---|---|

| GHG Emissions (Scope 1, 2, 3) | Yes | Often | Yes | Yes |

| Emissions Intensity | Yes | Yes | Yes | Yes |

| Board Oversight | Yes | Yes | Yes | Yes |

| Supply Chain Governance | Yes | Yes | No | Yes |

| Water Management | Yes | Sometimes | No | Yes |

| Diversity & Inclusion | Yes | Sometimes | No | Yes |

| Climate Scenario Analysis | No | No | Yes | Yes |

| Financial Materiality Assessment | No | Yes | Yes | Yes |

The overlaps are intentional. Core metrics like emissions, governance, and materiality are fundamental to all modern sustainability reporting frameworks.

The differences are in emphasis:

Your answer depends on three factors:

The good news is that frameworks are converging:

The trajectory is clear: ISSB will become the global baseline, GRI will remain for multi-stakeholder reporting, and SASB will provide industry specificity within the ISSB framework.

Managing four different frameworks manually is a data nightmare:

The solution: Build a single, authoritative dataset that maps to all frameworks.

Instead of maintaining separate GRI, TCFD, SASB, and ISSB databases, most enterprises now:

This approach eliminates data conflicts, reduces reconciliation burden, and ensures consistency across stakeholder communications.

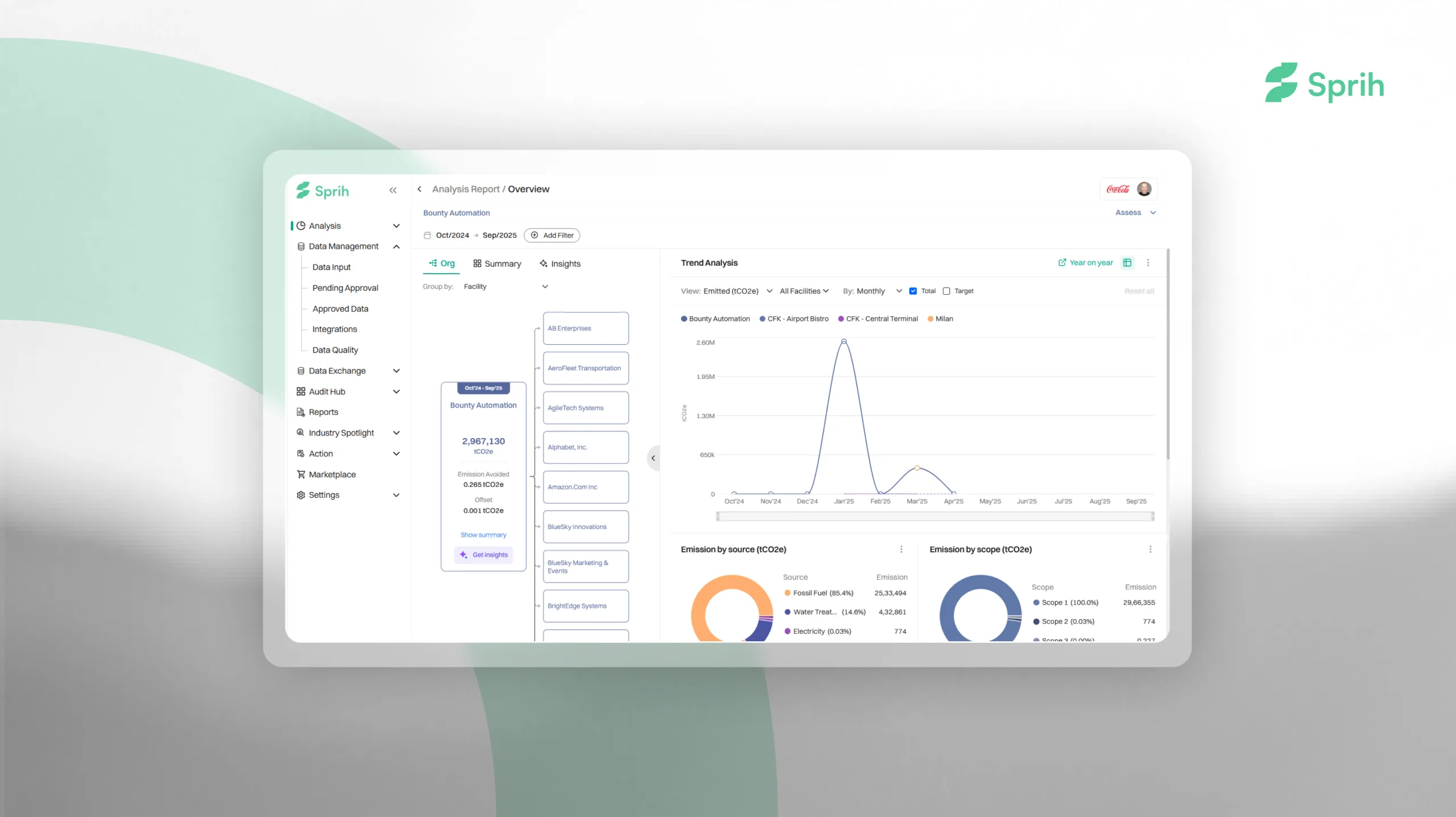

Sprih’s sustainability reporting platform is purpose-built for multi-framework sustainability reporting. Define your emissions data, sustainability metrics, and governance insights once. The platform automatically maps your data to GRI, TCFD, ISSB, CSRD, BRSR, and SB 253 requirements. Generate audit-ready reports for any framework in minutes without re-entering data or maintaining parallel systems.

Sprih’s intelligence engine understands GRI SASB TCFD ISSB framework equivalencies, data validation rules, and disclosure requirements for each standard, enabling your team to report confidently across all stakeholders.

For more framework guidance, see GRI Standards and IFRS ISSB resources.

For companies managing disclosures across multiple GRI SASB TCFD ISSB sustainability reporting frameworks simultaneously, Sprih’s sustainability reporting platform maps a single data set to all major frameworks automatically. Explore how Sprih’s AI-native sustainability platform eliminates the duplication burden of multi-framework reporting.

The sustainability reporting landscape won’t consolidate into a single framework anytime soon. Different stakeholders—investors, regulators, employees, customers—will continue demanding data aligned with their preferred standards.

The good news: the frameworks are increasingly compatible. GRI, SASB, TCFD, and ISSB now speak a common language around core metrics. The challenge is operational: managing data consistency across frameworks.

The solution: invest in platforms and processes that enable you to measure sustainability performance once and report it flexibly across multiple frameworks. This saves time, reduces errors, and ensures stakeholders always get consistent, accurate data.

Ready to simplify multi-framework sustainability reporting? Sprih enables you to report across GRI, TCFD, ISSB, CSRD, BRSR, and more from a single authoritative dataset. Request a demo to see how.