SECR UK Regulations are a cornerstone of the UK’s corporate sustainability framework. Designed to make carbon and energy reporting consistent and transparent, these regulations affect thousands of large UK organisations. If you’re a sustainability leader or CXO, understanding SECR is essential, not just to remain compliant, but to turn reporting into a strategic advantage. This guide walks you through everything you need to know.

SECR applies to large UK companies, both quoted and unquoted, as well as large LLPs. Your organisation must comply if it meets at least two of the following three criteria:

While college corporations and designated institutions (DIs) are technically outside the 2018 Regulations, they are encouraged to follow equivalent disclosures as part of best practice in sustainability reporting.

SECR is not just another reporting tick-box. It is designed to:

In short, SECR helps you cut emissions while building investor and public trust.

SECR reporting must include these five elements:

This includes:

All energy use must be translated into tonnes of CO₂ equivalent (tCO₂e), using government-issued conversion factors.

You must express emissions relative to a meaningful business metric, such as tonnes of CO₂e per employee. Use the same ratio year-over-year for consistent comparison.

Declare the method used to calculate emissions. Common frameworks include:

Clearly describe what your organisation has done to reduce energy use during the reporting period. If no action was taken, you must say so.

You should publish your SECR data on your organisation’s website by 31 March each year. Optionally, include it in your annual financial report.

If your data has gaps (e.g., no access to certain meters), note it explicitly. Explain what is missing and what steps you are taking to collect it in the future.

SECR uses the GHG Protocol’s scope framework to define emissions:

Scope 3 is optional, but highly recommended. It reflects growing pressure from investors to disclose full value-chain emissions.

If reporting at group level, include all subsidiaries unless they would be exempt individually.

If your organisation consumes energy under a PFI or lease agreement, you are still responsible for reporting that energy use, regardless of who pays the bill.

You don’t need external consultants. You can often use:

When exact data is unavailable, use reasonable estimates and clearly explain your assumptions.

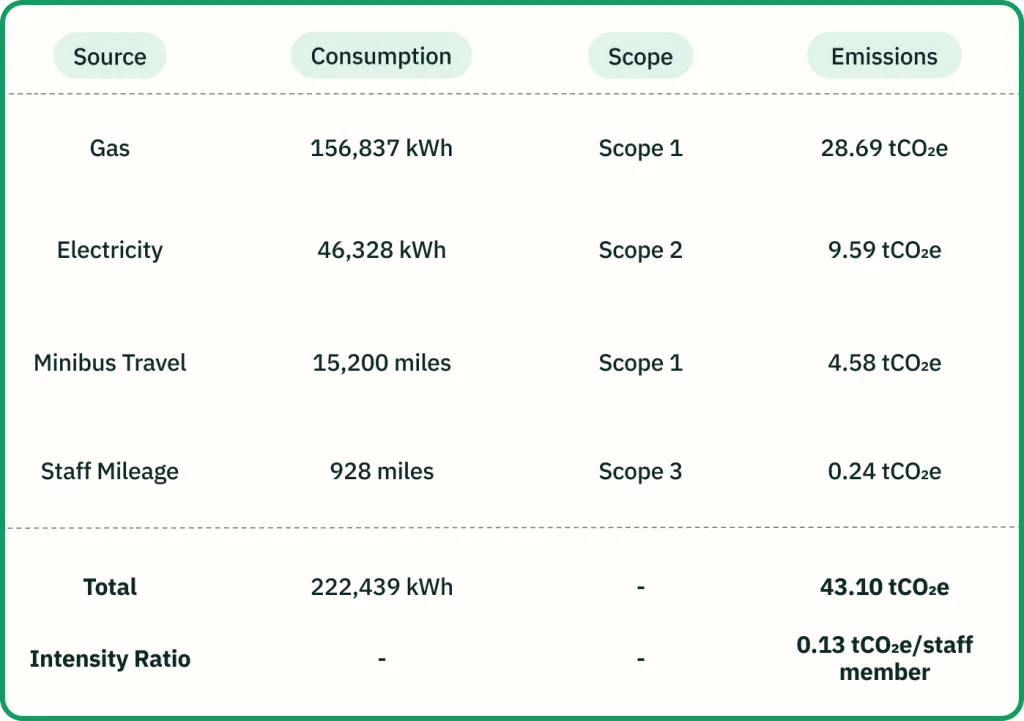

Here’s an example for reference:

Conversion factors should align with the most recent UK Government dataset.

High-quality disclosures:

Here’s an excerpt from a strong SECR disclosure:

“We reduced emissions by 8%, driven by replacing obsolete boilers and switching to smart meters. Our emissions fell to 0.13 tCO₂e per staff member, from 0.14 the previous year.”

If you’re new to this, you’re not alone. Here are helpful resources to support you:

Additionally, you may also find useful insights in recent Condition Improvement Fund bids or the DfE Energy Providers Framework.

SECR is more than a reporting obligation. It’s your opportunity to:

Sprih is making reporting effortless for companies, with an AI native platform that automates energy data collection, calculates your GHG emissions in real time, and generates compliant disclosures.

You can get a free consultation with our climate experts to help you plan your SECR disclosures and broader decarbonization strategy.

Secure your free consultation today. Get in touch.